- HOME

- Accounting Principles

- What is a cash flow forecast and what are the different types?

What is a cash flow forecast and what are the different types?

Cash flow forecasting is a way of predicting a business’s financial position by estimating the amount of money that is expected to flow in and out of the business. At a basic level, a cash flow forecast can tell you if your business has negative or positive cash flow at a given time.

Different types of cash flow forecasts

Short-term forecast: This forecast is done for the upcoming 30 days. It helps you identify whether there’s excess cash to invest towards business growth or there are emergency funding needs in the immediate term.

Medium-term forecast: This is done on a quarterly basis (covering approximately a 13-week window) and can be helpful in planning and budgeting operating expenses in order to improve business processes.

Long-term forecast: This normally spans between a year and five years. It is prepared as a reference for looking at the financial needs of the business and helps you gauge if there are any avenues for investment that would benefit your business in future.

Importance of cash flow forecasting

Accurate and timely forecasts help keep your business viable and prepare you for risks.

Here’s an example to consider. Let’s assume that you run a furniture business, and your customers have ordered goods worth $50,000 in March. You aren’t expected to receive the payment until April, however, because the invoice payment term mentioned is Net 30.

In the meantime, for March, you will need money to pay your bills and salaries while managing other expenses. This all adds up to $30,000. If you were relying on making enough revenue each month to cover expenses from that same month, you’d quickly run into an issue. By the time your March expenses are due, you will still be waiting for that $50,000 payment from the customer.

Of course, you have to account for every transaction for the month, so your income statement will reflect $20,000 of profit for March. But you won’t actually have it as cash to be spent until April. This creates a situation where you are profitable on paper, but your cash flow for March is still negative.

This scenario is just one of the many warning signals for a failing cash flow. With a robust cash flow forecast in place, you would know that running your business easily month to month requires at least $30,000 in cash to meet your fixed expenses. This allows you to plan ahead by saving some of the revenue from previous months.

Projecting your cash at the beginning of each month can help you prepare your business for any scenario. It can even help you make important decisions, like whether to take a business loan. Banks, investors, and others who are ready to lend your business money will want to examine your cash flow forecast, among other documents, before providing you with a loan.

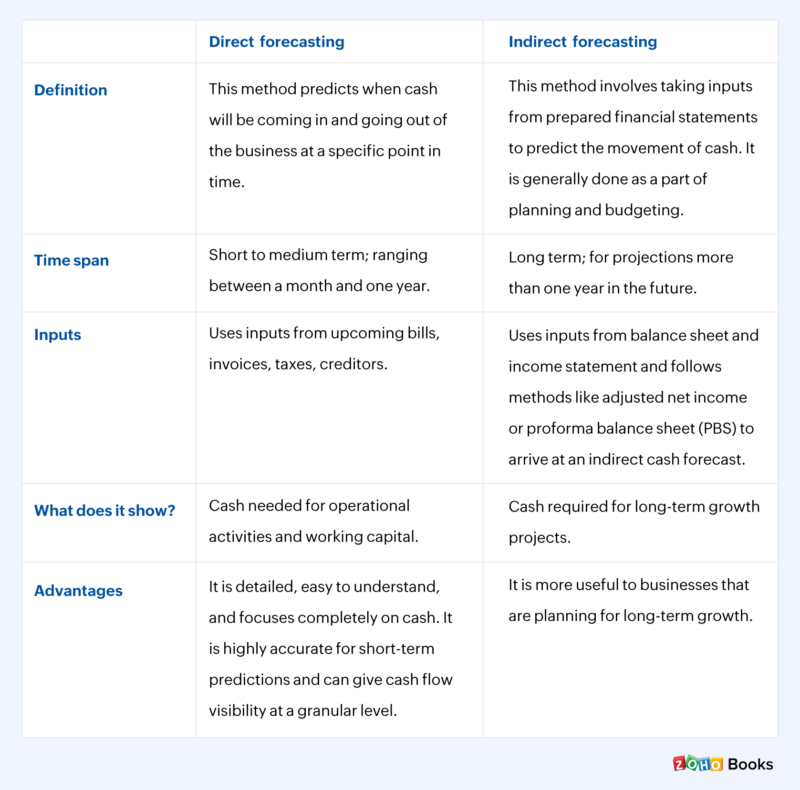

Methods of cash flow forecasting

There are two main methods of forecasting: the direct method and the indirect method. Both serve the same purpose of predicting the amount of cash that moves in and out of your business. However, the direct method focuses more on short-term and medium-term forecasts that give you an idea of whether there is enough cash for immediate needs. The indirect method is useful in long-term forecasts, which show the cash needed for the business to scale up.

The main takeaway is that there is no one correct approach as both methods have their own pros and cons. You may sometimes even need to combine the two approaches for better results.

Here are the differences between the two methods:

Elements of cash flow forecasting

Regardless of the method followed for cash projection, to create an effective forecast, you’ll need a record of your incoming cash, client payment terms, and projected costs.

Incoming cash

To forecast your cash flow, you’ll need to know how much cash you are bringing into your business. This usually includes cash coming from expected sales, loan advances, new capital, sales of assets, and accounts receivable.

The best place to start your forecast is to estimate your expected earning from sales for the weeks or months covered in your projection. Your past sales records are your best source of knowledge and act as important pointers to show your seasonal trends, ebbs and flows due to marketing, and more. Ideally, you would need at least 3 months worth of past sales data. If you don’t have that yet, your initial forecasts may not be as accurate as you would like, but they will improve over time.

Client payment terms

Once you’ve collected your estimated sales data, you need to note when you can expect to receive your payments. This is because when you make a big sale, the cash will not be available immediately for running your business.

For a typical business, a cash cycle is roughly 13 weeks, from the time your pay your suppliers for inventory to the time you collect your money back from the customers. A cash flow forecast needs to be at least one cash cycle long.

For example, even if your sales history indicates June to be a big month on sales, you may not realize the cash from these sales until July or August. Setting reasonable but relatively short payment terms during the sale—such as Net 30 or Net 45—is important for maintaining a positive cash position for your business at all times.

While forecasting, review the frequency of your payment collections and take delayed payments into account. If you typically receive a percentage of your payments late, then you need to note that in your forecast as well.

Projected cost

So far, your forecast accounts for the income you expect to make and your expected date of receiving your payments. Knowing your business spend is the last piece of the forecast puzzle. Some of your spend is likely fixed, while there are other parts which can be variable. Both need to be accounted in your projections.

Fixed costs are easy to list. They usually include rent, software licenses, and salaries of employees, which remain the same regardless of your earnings.

Variable costs, on the other hand, are unpredictable and are to some extent dependent on the sales you make. They include transaction fees, commissions, and changing costs of inventory.

Your fixed costs are pretty straightforward and can simply be added to the forecast. However, for your variable costs, you’ll want to use your historical records to try to figure out the trends of your irregular expenses so you can factor them into your forecast accurately.

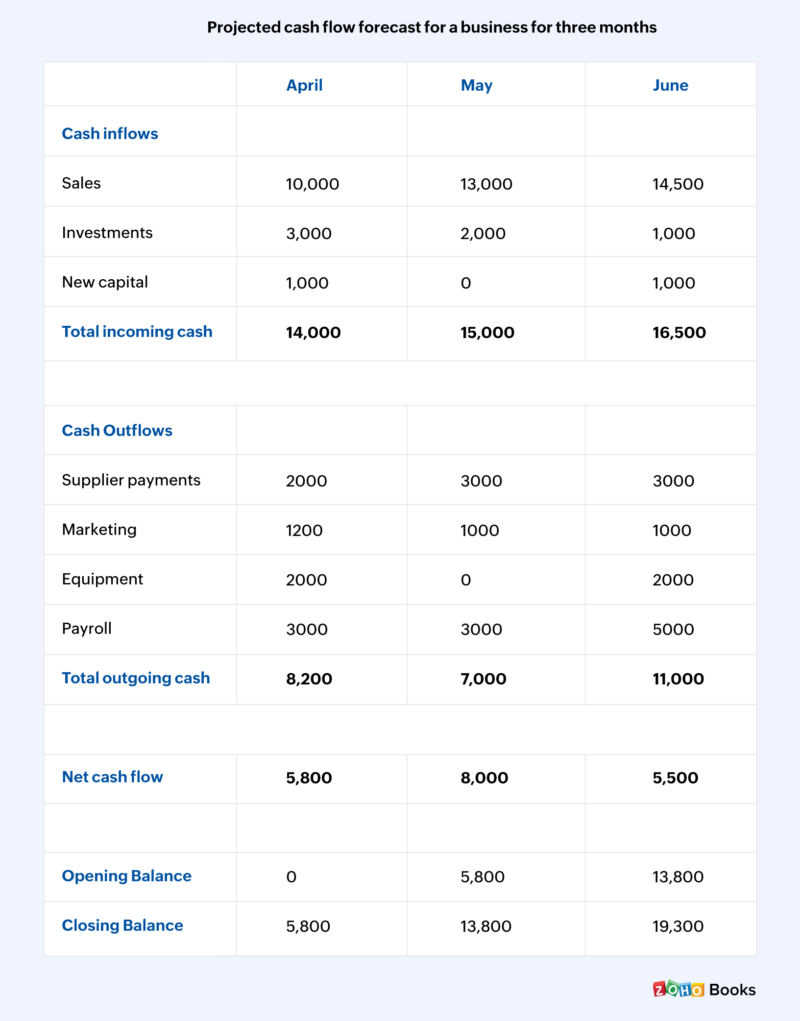

Example of cash flow forecasting

Here’s an example of what a cash flow forecast might look like for your business.

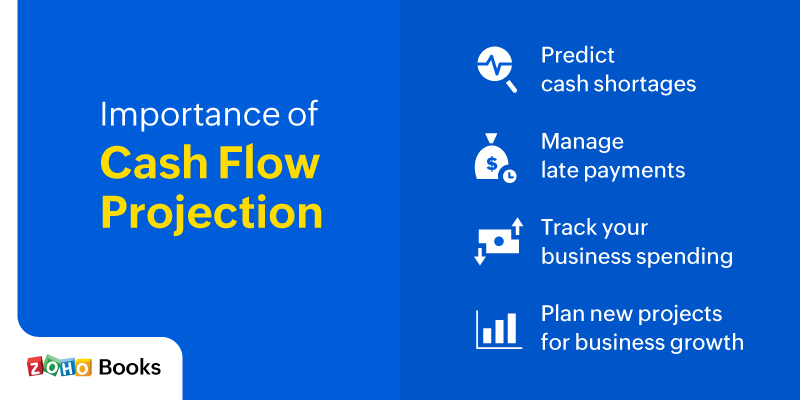

Advantages of cash flow forecasting

Cash flow forecasting can be an effective tool for your business, if used correctly. Some of its advantages are:

Predicting cash shortages: Forecasting helps you spot cash gaps well in advance and provides you with ample time to decide on a course of action to make up for the shortage. This helps you make informed decisions such as cutting down on your operational costs, putting expensive equipment upgrades on hold, changing customer payment terms, or looking for alternate financing.

Monitoring late payments: When you forecast, you will be able to predict the cash expected in your bank account if business goes as planned and then compare it with your receivables. If you observe a shortage of cash each month compared to what you expected, then you will know to look for the late payers on your list who are affecting your business finances. You can then plan to give them stricter customer payment terms or more effective credit control.

Tracking spending: Every growing business has time-sensitive goals to achieve, and forecasting helps by tracking outgoing cash from your business. It shows whether every activity is going according to budget and points out areas where you are overpaying or underbudgeting. It’s an important part of making effective budgets so that you can achieve your business goals.

Managing excess cash: It may be rare to see excess earnings in a business bank account. However, if your business does make some excess money, then you can think about investing in new markets or repaying loans that keep the business going. By forecasting, you can predict when you’re likely to have surplus cash in the bank and plan ahead what you’ll do with the surplus money.

Disadvantages of cash flow forecasting

Here are a few disadvantages of cash flow forecasting that can affect your business.

Limited power to predict business situations: When you analyze your businesses’ old cash flow data, you may notice that it’s affected by certain events or circumstances that fall outside the scope of your forecasting—like political changes, inflation, changes in the price of raw materials, or emergencies. Your cash flow statement may indicate that you are ready to face these challenges, but it is difficult to predict how and when these events will unfold.

No guarantees: A forecast is just a probability and cannot be 100% accurate all the time. You can make important financial decisions like investing in new equipment by referring to your long-term forecast. However, there’s no guarantee that purchasing this equipment will give you the anticipated result and increase your revenue. Even with a forecast, you’re still vulnerable to unexpected changes to your cash flow, and they can still affect the financial health of your business.

Conclusion

Forecasting is an attempt to estimate the future growth of your business by analyzing data from past events. Understanding and predicting the cash coming in and going out of your business can help you make smart decisions and plan in advance to avoid a cash crisis. Having a rough estimate of how your business is likely to do every month gives you an idea of where to spend, how to save, and where to invest in your business today.

The main challenge with forecasting is that it is only effective as long as the data is relevant and up-to-date, and it is not a simple task to accomplish on your own. Businesses often use spreadsheets as a quick fix for smaller forecasts, but the process is complicated and there is a huge scope for making errors.

The easiest way to stay on top of your financials is by using an online accounting solution that can help you monitor incoming and outgoing cash. You can note payments on invoices, manage expenses, and balance your accounts, all in one place. A real-time overview of your cash can help you check whether your business is able to stick to its budget, and to ensure that there’s enough time to rectify problems before the business goes off track.