- HOME

- Taxes & compliance

- Supply under VAT in the United Arab Emirates

Supply under VAT in the United Arab Emirates

What is a supply?

A supply refers to goods or services that are exchanged for consideration. A supply occurs when there is a transaction between two persons and at least one of them is a registered taxpayer. Buying, selling, and stock transfers are all supplies, even if there is no exchange of money.

You can also think of a supply as a transfer of goods or services between two people in the UAE, in which the goods or services that are supplied are meant to advance the business of at least one person involved in the transaction. It can mean buying goods for selling them, outsourcing a service, conducting imports or exports, and more.

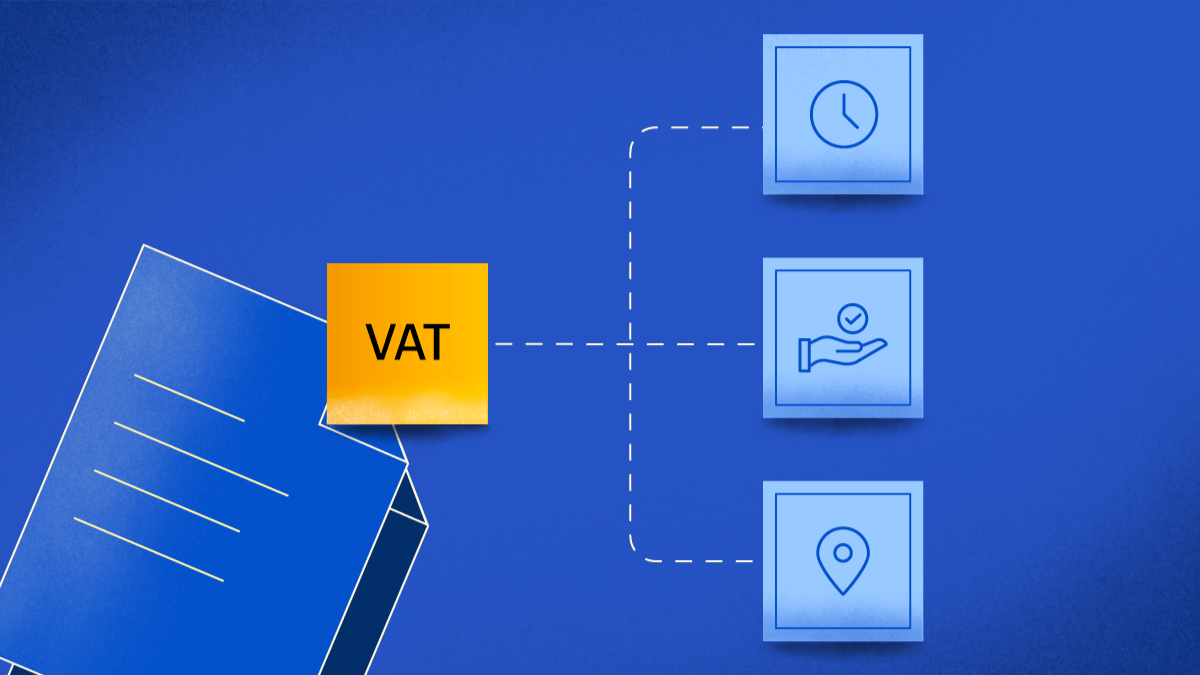

What are the components of supply under VAT?

A supply under VAT has three attributes that are used to calculate the tax owed for the transaction: place, value, and time.

- Place of supply - This component determines whether the supply is made in or outside UAE for VAT purposes.

- Value of supply - This determines the taxable value of the supply and the amount of tax that has to be paid for it.

- Date of supply - This component determines what VAT period the transaction falls under.

Types of supply under VAT

Under the UAE VAT, supplies can be classified as:

Standard rated supply

The standard VAT rate of 5% will be applied to almost all goods and services in the UAE. The standard rate will apply to the sale and lease of commercial property, hotel and restaurant service, repairs and maintenance services, and more.Zero rated supply

Zero rated supplies are taxed at 0%. The invoice for a zero rated product should include a tax column showing a zero rate and zero value. The reason for showing the zero value in the invoice is to ensure that this transaction is not used to claim tax offsets later.

However, if you purchase an item for which the tax has already been paid and later the item is sold, you are eligible to claim the tax credits for your purchase.

For example, if you purchased the raw material for baking a cake and paid tax on it, and later sold the cake without charging tax on it, then you can claim back the VAT you paid.

Exports, healthcare, medicines, and medical equipment are examples of zero rated supplies.VAT-exempt supply

Supplies which are unaffected by the VAT implementation are known as exempted supplies. No tax will be charged for such supplies, and any tax which was previously paid on their purchase will not be available for credit.

Let’s consider a bus service, which is categorised as a local passenger transport. Local transports are tax exempt, so the bus service cannot collect any VAT from the passengers. Because it does not collect any tax, it can’t get credit for the tax that it paid for the purchase of the bus.

Educational institutions, pharmaceutical supplies, and financial services are examples of VAT-exempt supplies.Out-of-scope supply

If an overseas supplier or a non-registered entity supplies goods or services to an overseas person, these supplies will be considered out-of-scope for VAT in the UAE.

For example, local confectionery company A sells candies to local company B. The candies are shipped directly from Company A’s factory in Singapore to Company B’s branch in London. The goods do not pass through the UAE, so the sale of these candies is an out-of-scope supply.

There are two basic kinds of out-of-scope supply:

(i) When goods are imported from an overseas supplier and sold to an overseas buyer, without being brought into the UAE, it is considered out-of-scope. This is also known as merchant trading.

(ii) If a VAT-registered person in the UAE supplies goods or services to a VAT-registered person in another GCC state, the sale is said to be outside the scope of VAT.

Deemed supply

A deemed supply will occur when a business purchases something, claims input VAT for it, and later puts the item to a non-business or private use. Examples include gifts and motor fuel for personal use.

When a VAT-registered business deregisters, any goods held by the business for which the input tax has already been recovered are treated as deemed supplies.Composite supply

A composite supply occurs when two or more goods or services are sold together as a set. To qualify as a composite supply, the items cannot be sold individually. The VAT rate on a composite supply is determined by the principal component.

Application of VAT on Goods and Services

When the supply of goods or services happens partly before and after the date of VAT implementation, there are a few factors to keep in mind before deciding whether VAT is applicable on the supply or not.

Goods

| Supply | Payment | Is VAT applicable? |

|---|---|---|

| Supply of goods before 2018 | Payment made in 2018 | No |

| Supply of goods in 2018 | Payment made before 2018 (partial or full) | Yes |

Services

| Supply | Payment | Is VAT applicable? |

|---|---|---|

| Supply of services before 2018 | Payment made in 2018 | No |

| Supply of services in 2018 | Payment made before 2018 (full) | Yes |

| Supply of services partly in 2017 and 2018 | Payment made before 2018 | Only on services in 2018 |

Contracts

In case of contracts, VAT can be accounted by the supplier or the recipient. Let’s look at cases where this would be applicable.

| Amount in Contract | Who pays VAT? |

|---|---|

| Exclusive of VAT | VAT is paid by the Recipient |

| Inclusive of VAT in the contract | VAT is paid by the Supplier |

In case the contract does not mention VAT, then the amount is treated as inclusive of VAT.

If the recipient is registered for tax and able to recover it, then the amount is treated as exclusive of tax.